Between attracting top talent and keeping your employees in good health, making sure your workforce has solid insurance is vital to the success of your business — but it comes at a price. And when you add spouses into the mix, you might see those dollar signs multiply. Some employers have responded by barring spouses from joining employee health plans, but doing so can come at its own cost, potentially alienating married members of your workforce.

If you’re eyeing your health care expenses and considering a new strategy for spouses, introducing a spousal surcharge could offer a workable compromise, allowing employees to share coverage with their partners without blowing a hole in your company’s budget. Spousal Surcharge Trends According to Anthem’s Trends in Health Benefits report, most employers — both large and small — still offer health benefits to spouses and dependents. But a growing number are changing how they factor spouses into their benefits offerings. The 2018 International Foundation of Employee Benefits Survey found that, up from 16 percent in 2016, just over 20 percent of employers now either charge employees more to add a spouse to their health plan or exclude spouses entirely. For example, a spouse may be charged an extra fee, say $100 a month, if they want your company’s insurance. Some only charge or exclude spouses who have coverage available elsewhere, while others have blanket policies for all spouses. Reasons for Implementing a Spousal Surcharge Should your business create similar boundaries around spousal health insurance coverage? Some employers take these measures because of rising health care costs. They still want to offer good medical coverage, but the expense pushes them to decrease the number of spouses signing up for coverage if they have other viable options. There are other ways, of course, that employers can attempt to offset rising health care costs, such as offering high-deductible plans. But sometimes that’s not enough, and the most cost-effective option is still to reduce — or at least change — spousal coverage. In those cases, it might be a good option to implement surcharges. Sometimes the charges are necessary in order to to keep premium increases as low as possible. How to Communicate Changes If you decide to implement boundaries to spousal benefits, you’ll need to communicate these changes clearly to your staff without alarming them unnecessarily. The best approach is just to be transparent and honest about why you’re making this change. Explain that you want to offer good insurance while keeping premiums low, and that you must implement the surcharge in order to continue offering affordable insurance to those who need it the most. While you should communicate this first in writing, offer employees a chance to meet one-on-one to ask questions. Make sure to communicate the change far enough in advance that each of your staff members has time to research their spouse’s insurance options. In some cases, it might be helpful to hire a third-party company to run a verification process for everyone currently on your plan. To keep morale up and express goodwill, consider including exceptions when you implement the surcharges rather than charging all spouses across the board. Exceptions can include spouses who don’t have access to insurance anywhere else, spouses eligible for Medicare and spouses whose employer’s plan doesn’t meet specific standards. Keeping health care costs down isn’t always easy for employers or employees. When you seem to be stuck between cutting spouses out of your benefits offerings and putting your business’s bottom line at risk, the middle ground may be the best place to land. When it comes to health insurance for small business owners, it’s important to do your homework. They could be a good option for certain businesses and self-employed individuals, but be sure to consider both the plans’ advantages and disadvantages before making a decision.

0 Comments

Not long ago, offering domestic partnership health benefits was a way for employers to equalize benefits for employees in same- and opposite-sex partnerships. But landmark legislation and new trends have changed things.

After the Supreme Court’s 2015 Obergefell v. Hodges ruling legalized same-sex marriage nationwide, the percentage of employers offering health benefits to domestic partners declined. If a spouse is now a spouse, the thinking goes, there’s no longer a need to offer specific benefits to ensure that employees with same-sex partners have access to the same level of benefits as employees with opposite-sex partners. But employers are wise to think through all of the considerations before dismissing benefits like domestic partner health insurance. Offering benefits to same- and opposite-sex domestic partners allows your organization to cast a wider, more inclusive net for attracting and retaining a highly skilled workforce, promoting diversity and setting your organization apart from the competition. If you’re deciding whether to add domestic partner benefits to your company’s offerings, here are three important factors to keep in mind. 1. Your State May Have Its Own Requirements for Employers There’s no federal law requiring employers to offer benefits to spouses or domestic partners. However, most offer benefits to spouses anyway. Past the federal level, some states have stepped in with their own stipulations, requiring state-regulated health plans to extend benefits to domestic partners if benefits are offered to spouses. What constitutes a domestic partnership? Rules on this vary from state to state, too, but in states or cities that don’t have written definitions or official domestic partner registries, employers that offer domestic partner benefits should clearly define what constitutes a domestic partnership. This helps ensure that there’s no ambiguity in terms of who is eligible for coverage and that coverage is offered consistently to all eligible employees. 2. Your Employees Will Need to Keep Up With IRS Regulations Health insurance benefits are generally not subject to taxes, but that’s often not the case when it comes to coverage for domestic partners. Unless the domestic partner is actually the employee’s tax dependent, the fair market value of the domestic partner’s coverage is taxable and has to be added on the employee’s W-2 as part of their total taxable compensation. In addition, unless the domestic partner is the employee’s tax dependent, the domestic partner’s medical expenses cannot be covered using the employee’s health savings account (HSA), health reimbursement arrangement (HRA) or flexible spending account (FSA). That’s according to IRS rules, which allow those accounts to be used for spouses and tax dependents but not for domestic partners. So if an employer offers a tax-advantaged account in conjunction with a health plan and allows domestic partners to be covered under the health plan, it’s important to help employees understand how the funds in the tax-advantaged account can and cannot be used. 3. Tracking the Trends Could Give You a Competitive Edge Benefits packages are more than just a nice add-on for employees — for many people, they’re as important (or even more important) than the salary they’ll make at a company. In a recent poll, 80 percent of people said they’d take a better benefits package over an improved salary. The high stakes surrounding benefits encourage most employers to go beyond the bare minimum when it comes to spouses: Even though the Affordable Care Act doesn’t have any requirements concerning spousal or domestic partner coverage, most employers that offer health coverage do extend benefits to the spouses of eligible employees. Less than half offer domestic partner benefits. So to have a competitive benefits package, it may be wise to consider offering benefits to domestic partners. The cost to do so is typically minimal, as uptake of domestic partner benefits tends to be very low on the whole. There’s no clear-cut answer in terms of whether an organization should offer health benefits to domestic partners, and employers considering this benefit should discuss the tax implications with their accountant. But having the coverage available as an option could end up being the factor that helps an organization recruit a diverse staff of top talent, regardless of their domestic situation. Your Chip eligibility is based on your household size and income and determined by the government and you can apply any time of year.  When Form 1095-A arrives in your employees’ mailboxes, you might find them turning to you for help in understanding what the form is all about and what they need to do with it. That’s particularly true if your small business offers a qualified small employer health reimbursement arrangement (QSEHRA) and you’re helping employees pay for the health insurance plans that they’re purchasing for themselves.

If you’re facing questions and don’t have the answers to them, here’s what you need to know to cover the basics. What Is a 1095-A, and Why Did Your Employee Get One? If your employee receives this form, it means they had health insurance coverage via the health insurance exchange, also known as the Marketplace, for at least one month of the previous year. The forms come from the health insurance exchange — in most states, the exchange is HealthCare. gov, although 11 states and Washington, D.C., run their own exchanges and send out their own forms. The form is sent to the person who enrolled in the plan through the exchange, and the IRS gets its own copy. This form is essentially a place to collect information. It shows the name of the person who enrolled in the exchange plan as well as any covered family members. For each month that the plan was in effect, the form shows the total premium for the plan and the amount of premium tax credit that was paid on the enrollee’s behalf (or, in other words, sent directly to the insurance company to offset the employee’s premiums). The form also says how much the second lowest cost silver plan (SLCSP) would have cost if the person had selected that plan. If that’s actually the plan in which the person was enrolled, the premium for their plan and the premium for the SLCSP will be the same. What Does Your Employee Need to Do With the Form? If your employee benefited from a premium tax credit, or if they paid full price for their plan but want to claim the tax credit on their tax return, the information on this form is vital. There’s another form that then comes into play — Form 8962. Just like with other forms your employees might receive, like W-2s and various 1099s, the employee will keep the form they get from the exchange for their own records. But they’ll use the information on it to complete Form 8962, which they’ll file with their tax return. If your employee paid full price for the plan they purchased in the exchange and they’re not eligible to claim the premium tax credit on their tax return, they don’t need to complete Form 8962. In that case, they don’t have to do anything with the information on their 1095-A. Assuming they had health coverage for the full year, they can check the box on their 1040 that says “full year health care coverage or exempt” and carry on with the rest of their return. Have employees who are wondering whether they’re eligible for a premium tax credit to offset the cost of the plan they purchased in the exchange? Point them toward their household’s modified adjusted gross income (MAGI) — but make sure they’re using Affordable Care Act-specific calculations, since this isn’t the same as normal MAGI. To be eligible, their MAGI can’t exceed 400 percent of the prior year’s poverty level. For example, for 2018 coverage, they’d use 2017’s poverty level for comparison. They also can’t have had access to an employer-sponsored plan that was affordable and provided minimum value. Assuming a premium tax credit was paid on the employee’s behalf — or they paid full price and wish to claim the premium tax credit on their return — they’ll complete Form 8962 using the information provided on their 1095-A. Premium tax credits that are paid throughout the year on behalf of exchange enrollees are calculated in advance based on the enrollee’s projected MAGI. However, the tax credit amount then has to be reconciled based on their actual MAGI, as determined by their tax return. The premium tax credit is the amount necessary to keep the SLCSP at a level that’s considered affordable based on someone’s MAGI. Regardless of which plan a person actually buys, the premium tax credit is based on the price of the SLCSP — meaning premium tax credit amounts differ between enrollees, since the cost of the SLCSP varies based on age and location. If you offered a QSEHRA and your employees used those funds to buy coverage in the exchange, they’ll receive 1095-A forms just like any other exchange enrollee. But the IRS has specific rules for premium tax credits when the person is also receiving a QSEHRA benefit, and QSEHRA benefits’ impact on premium tax credits depends on each person’s specific situation. The details are clarified in this set of IRS FAQs. What About Forms 1095-B and 1095-C? When your employees ask about Form 1095-A, you — and they — might wonder how these forms differ from 1095-B and 1095-C. All three forms were created as part of the implementation process for the Affordable Care Act, and they’re all designed to document the health coverage that a person had during the year. In the case of a 1095-C, it also shows the health coverage offered to the employee, even if they never ended up taking it. Form 1095-B is sent out by insurance plans that cover people who didn’t buy their plan through the health insurance exchange. This includes government entities like Medicare, Medicaid, the Children’s Health Insurance Program (CHIP) and commercial plans in the individual and small-group market. Form 1095-C arrives via applicable large employers (ALEs), indicating the coverage that was offered to each employee and whether the employee enrolled in the plan. All of these forms are sent to both the plan enrollee and the IRS. In some cases, an employee will receive more than one of these forms for a given year — for example, a person would receive all three forms if they were employed by an ALE from January through June (1095-C), covered under an exchange plan from July through September (A) and then covered under a small employer’s group plan from October through the end of the year (B). Tax season can easily become a puzzling flurry of forms, and eventually they all start to sound the same. Save your employees from confusion by ensuring they have the know-how to keep all of their papers straight. A lower premium of chip health insurance pa is not a benefit for patients with a chronic or life-threatening illness that requires a great deal of medical oversight, treatment and routine prescription medications.  As employees approach the end of their careers, it’s likely that most of them will have questions about retirement health insurance. The specifics will vary from one person to another, particularly in terms of Medicare eligibility, which begins at the age of 65 for most people — though about 16 percent of the 60 million Americans with Medicare are younger and eligible due to a disability. An employee who’s retiring at 55 will probably have different coverage needs and questions from an employee retiring at 65 or older.

Here’s a look at some of the most common concerns and questions people have when it comes to retirement health insurance. Help Your Employees Know Their Coverage Options What coverage will your employees have after they transition to retirement? Will they need to purchase their own? Are they eligible for Medicare? Does your employer-sponsored plan extend to retirees? Employer-Sponsored Group Plans If an employee retires prior to age 65 and your group plan offers retiree coverage, that might be all the coverage they need until they turn 65 and transition to Medicare. At that point, the employer-sponsored retiree plan will become secondary, and Medicare will be their primary coverage. For employees who are still working after they hit 65, Medicare can be primary or secondary to the employer-sponsored plan, depending on the size of the employer; once that employee retires, Medicare becomes their primary coverage even if they retain retiree coverage through your group’s plan. Individual Plans If your group plan does not extend coverage to retirees, employees who retire before age 65 will need to obtain their own coverage from the individual insurance market unless they have access to coverage under their spouse’s plan. For plans purchased in the state small business group health insurance exchange, there are premium subsidies available to offset the cost of coverage as long as the enrollee’s household income doesn’t exceed 400 percent of the poverty level. For lower-income enrollees, there are also cost-sharing reductions that help to lower the out-of-pocket costs on silver plans. There’s an annual open enrollment period each fall for health coverage purchased in the individual market, but an employee who retires and loses their employer-sponsored coverage will have access to a special enrollment period during which they can sign up for a new plan mid-year. Medicaid Medicaid is also a coverage option that might be available to some employees who retire prior to age 65. The majority of states have expanded Medicaid under the Affordable Care Act, making coverage available to adults up to age 64 whose household income doesn’t exceed 138 percent of the poverty level. Eligibility for expanded Medicaid doesn’t depend on assets; only income is considered — but enrollees should be aware of how Medicaid estate recovery works in their state. Medicare For employees who transition to retirement at age 65 or older, Medicare will likely become their primary retirement health insurance. Medicare has several different components and coverage options.

Help Retirees Avoid Penalties As of 2019, there is no longer a federal penalty for being uninsured — although Massachusetts, New Jersey and Washington, D.C., have their own state-based penalties for people who go without health coverage, and Vermont will join them in 2020. But there are some penalties that apply specifically to Medicare enrollees if they delay their enrollment without having creditable coverage from an employer-sponsored plan. This is important for retiring enrollees to understand if they’re eligible for Medicare — or will be soon — and are considering initially skipping some parts of Medicare coverage. Medicare Part A is premium-free for most enrollees, but Medicare parts B and D have premiums, and healthy people sometimes wonder if they’d be better off delaying their enrollment in those parts until they need health care. There are annual enrollment windows for both parts, so it’s possible to delay enrollment in Part B and Part D and then sign up later. But unless an employee has coverage from an employer- or union-sponsored plan during the time that they delay their enrollment in parts B or D, they’ll end up with a penalty if and when they do eventually enroll. Here’s how the penalties are calculated:

So, if an employee will have employer-sponsored retiree coverage — either their own or a spouse’s — then they may be able to delay enrollment in Part B and D. But if not, enrolling in both parts upon turning 65 is generally the best approach. This retirement planning guide from the federal government is helpful for employees who are working through these decisions as they prepare to retire. Although there isn’t technically a penalty associated with delayed enrollment in Medigap plans, it’s important to understand that Medigap insurers in most states can use medical underwriting to determine eligibility for Medigap plans if a person applies for coverage after their initial six-month open enrollment window ends. So, a person with preexisting conditions might be unable to obtain Medigap coverage (or have to pay more for it) if they delay their enrollment.  As value-based approaches to care have gained traction, health care staffing has become more efficient. In the last few years, a trend of medical upskilling means that nurse practitioners and physician assistants have taken on tasks that doctors once performed, allowing physicians to focus on the duties for which they alone are qualified. It’s a more efficient use of resources, and it’s more professionally satisfying for everyone involved. Now, medical assistants (MA) are taking on some of the tasks formerly performed by nurses. With physician shortages growing, all of this adds critical capacity to the health care team.

This “task shifting” moves routine tasks to lower-skilled professionals, according to the Harvard Business Review. In health care, this is often termed “working at the top of one’s license.” The challenge is to ensure that the person is qualified for the task being assigned. That’s where upskilling the workforce comes in. Medical upskilling is not a completely new concept, but it may be more important now than ever before. This is the year health care organizations — incumbents and disruptors alike — will identify which employees need to be upskilled, consulting firm PricewaterhouseCoopers (PwC) predicts. This will occur “from the back office to the front lines and all the way up to the C-suite.” As with almost every business today, technology is driving the need for new training. Artificial intelligence, robotics and other technologies will create value by improving telehealth and reducing “transactional tasks,” according to PwC. But it won’t happen without training. In fact, 45% of provider executives surveyed by PwC said the capabilities of their workers are a “significant barrier to organizational change.” MAs on the Front Lines Such concerns are one reason MAs are being trained to perform some of the tasks delivered by nurses, including new roles in health IT and patient engagement — especially coaching. Training programs abound, from community colleges to nonprofits focused on cultivating primary care teams. Patients — your employees — are more likely to see this happen on the front lines. Allowing MAs to take on tasks previously performed by registered nurses (RNs) obviously saves money, but it also means that patients aren’t rushed through health coaching. The physician or RN may not have the time to sit down with patients to provide adequate coaching and support — and if they did, it would be considerably costlier. Addressing Social Determinants of Health It’s here that community health workers can play a role as well. Social determinants of health, from income and education to housing and access to food, play a significant role in health care costs and outcomes. The American College of Physicians estimates that these health disparities result in $309 billion in economic losses each year. Community health workers (CHWs), a relatively new addition to the health care team, are helping provider organizations address these issues early. CHWs often don’t have a medical background, but they frequently do have roots in the community. They may go shopping with a patient to help them select healthier food, or connect patients with transportation or social services. A physician can’t spend as many hours talking about nutrition, transportation or unpaid electric bills. The Centers for Disease Control and Prevention offers a wealth of resources to train CHWs. With the right medical upskilling, they can specialize in a specific area, such as maternal health or stroke prevention. Better Skills, Better Connections, Greater Value Home health aides provide value similar to community health workers. According to Health Affairs, if high-quality care can be delivered in the home, it keeps costs down, makes life easier for patients who may have trouble getting to a physician and keeps patients out of the hospital. For example, Health Affairs reports that training 6,000 home care workers in California contributed to a 41% decline in the rate of repeat emergency department (ED) visits and a 43% decline in the rate of rehospitalization. The result: savings of up to $12,000 per patient. Similarly, home health workers in New York City received 200 hours of training in chronic diseases, among other things. After the training, they were designated Care Connections Senior Aides. They then made home visits to support the on-the-job upskilling of hundreds of other home-care workers. The bottom line? An 8% reduction in the rate of ED visits, as well as improved job satisfaction among home care workers. Don’t let the term “medical upskilling” mislead you. Yes, health workers are learning new skills, but health systems are also capitalizing on these workers’ existing competencies — and their relationships with patients and caregivers. Medication Management on the Team Finally, let’s look at pharmacists. Pharmacists can take on an array of tasks often left to physicians or nurses, including diabetes, hypertension and depression management, as well as new medications and dosage change. They can also review “polypharmacy” issues, which arise when a patient’s numerous drugs prescribed by multiple clinicians may interact badly with each other. And pharmacists can help patients gradually come off opiates. The model can work in a variety of ways, from onboarding a clinical pharmacist as part of the practice staff to collaborating with a community pharmacist to working more closely with pharmacists within a particular health system. Clinical pharmacists may need medical upskilling and certification to provide what’s called comprehensive medication management (CMM). Some pharmacy schools offer CMM-based certification programs for pharmacists. CMM often targets the most complex — and most costly — cases. And again, the pharmacists can spend more time with patients; in this case, they’re better-suited to talk about medications. As with the other examples, CMM reduces physician workload. Moreover, it has resulted in demonstrated reductions in ED and hospital admissions. As CMM shows, medical upskilling isn’t limited to lower-paid health workers. Finding the best individuals for a particular set of tasks is simply a more efficient way to work. It controls costs, supports better outcomes and improves both patient and professional satisfaction. Check the chip guidelines carefully before exploring the CHIP programs, this will help you to find best plans for your child.  Long-ago miscalculations by insurers have led to policyholders’ facing steep premium increases. But there are ways to keep costs down.

Karen Herzog, a retired high school teacher, bought a long-term care insurance policy 12 years ago because she didn’t want to burden her only daughter if someday she could no longer care for herself. Then a letter arrived in May that complicated her well-laid plan. Her monthly costs would double within two years, reaching nearly $550 — a significant portion of her fixed income. “Many of us will be forced to drop this policy,” said Ms. Herzog, 73, of Ocala, Fla. “This was supposed to be my parachute.” Ms. Herzog reluctantly started paying a higher monthly premium while she weighed her options. But her insurer, Genworth — the nation’s largest provider, with 1.1 million long-term care policyholders — said she might face another rate increase in eight years, when she’s 81. Long-term care insurers have been imposing significant rate increases for nearly a decade, and the problem has the attention of the regulators in each state, who must approve premium increases. The regulators’ national group created a task force earlier this year to address the issue, although the effort probably won’t provide much relief to people like Ms. Herzog. “There is an inherent tension as a regulator,” said Scott A. White, the Virginia insurance commissioner and chairman of the task force. “You want to protect consumers against rate hikes, but you also want to make sure the carriers remain solvent and are able to pay claims into the future.” Long-term care insurance can fill an important niche for many retirees. It covers what Medicare generally does not: long nursing home stays, health care aides at home, adult day care and parts of assisted living. Wealthier individuals can often pay for these costs on their own, while those with little money usually lean on Medicaid. The most common benefits — which are generally paid in the form of a daily benefit, say $150 — pay for care at home, according to Bonnie Burns, training and policy specialist at California Health Advocates, a consumer advocacy group. Those who bought policies had good reason: About half of Americans turning 65 will develop a disability serious enough to require long-term care services, according to a 2016 federal report. Most will need assistance for less than two years, but about one in seven will need it for more than five years. Why are premiums swelling so much? There were several factors, but two of the more serious problems involved the predictions insurers made roughly two decades ago. Not only did they underestimate how long policyholders would live, they overestimated how many people would drop their policies, which meant insurers would not have to pay claims. The financial pressures have left only about a dozen companies selling new coverage, down from more than 100 in the market’s heyday. For many existing policies, they’re seeking rate increases. But not all states have granted them, which Mr. White said meant policyholders in certain states are subsidizing those in others. The task force is hoping to address the unpredictability and lumpiness of these pricing shocks. But that’s little comfort for policyholders who have already received notices for price increases. Regulators approved higher premiums on at least 84,000 policyholders at Genworth alone during the second quarter, according to a sampling of filings recently analyzed by S&P Global Market Intelligence. Deciding whether to renew one of these policies can feel like an impossible calculation, and there’s a lot to consider. Insurers generally provide policyholders with several options in between accepting a full rate increase and canceling the policy. “Not every company is doing the same thing in the same way and when they present these options to consumers, they are totally confused by them,” Ms. Burns said. “But they can reduce the effect of the rate increase.” As hard as it may be to accept, it could make sense to pay the higher rate if you can still afford it. Buying a similar policy would likely cost far more now, and the same level of coverage is often not available (if you’re even still insurable). “It’s technically still a deal relative to what coverage costs today,” said Michael Kitces, director of wealth management at Pinnacle Advisory and publisher of the Nerd’s Eye View blog. But many people won’t be able to absorb the full increase, so cutting benefits may be the next best option. That can include reducing the period for which the policy pays benefits, the daily amount of the benefit, and the inflation rate at which the daily benefit grows. Mr. Kitces suggests considering the cuts in a certain order. If your policy pays benefits for more than five years, consider shaving that back first, since few people need it that long, he said. If you still want to reduce your premium, your choice could depend on your age. If you’re in your 70s or 80s — or have held the policy for a while and have already seen benefits grow — consider reducing the inflation rate. If you’re in your 50s or 60s, you might be better off reducing your daily benefit rate, particularly if that amount is higher than the typical cost of care in your area, and letting it grow with inflation. Your insurer might be able to offer other solutions if you ask. “You can call and sometimes they will be flexible with giving you other options that were not in the package sent in the mail,” said Jesse Slome, executive director of the American Association for Long-Term Care Insurance, a trade group. If you simply cannot afford to pay any longer, you might not have to walk away with nothing. You may be able to convert your old policy to a new one that is worth the amount of premiums you already paid. Ms. Burns, from the advocacy organization, said she worried that some insurers could steer people to this option because it reduces their liability. That’s why she encourages people to seek help when re-evaluating your policy. She suggests contacting a counselor through your state’s health insurance assistance program. The lingering effects of the industry’s early miscalculations have made some policyholders — including Ms. Herzog — worried about their insurers’ long-term viability. (Genworth, which agreed in 2016 to sell itself to the investment firm China Oceanwide, said carriers were required to set aside a certain level of assets to support their ability to pay claims.) “We’ve had more companies get out of business than are in it, and they are still paying legitimate claims,” said Brian Gordon, president of MAGA Long Term Care Planning, “We are still very comfortable even though some of them are not writing new policies.” Insurance company failures are rare, but the long-term care world does have a recent example: Penn Treaty was liquidated in 2017. But experts point out that Penn didn’t have other lines of business to offset its problems, like many other providers do. Should a long-term care insurer end up like Penn Treaty, state guaranty associations generally provide at least $300,000 in benefits for policyholders through a safety net that is funded in part by other insurers, according to the National Organization of Life & Health Insurance Guaranty Associations. But for the majority of policyholders, the biggest worry will remain price increases. The regulators’ task force may work to even out the differences in increases experienced by policyholders across different states, but that could mean higher costs for people who have thus far been spared. “Long-term care is a problem for the whole U.S. and for many seniors who paid into these policies,” Ms. Herzog said. “I live alone. Who is going to take care of me? Your Chip eligibility is based on your household size and income and determined by the government and you can apply any time of year.  There’s surprisingly little rigorous research on programs like Medicaid and Medicare. A few years ago, Oregon found itself in a position that you’d think would be more commonplace: It was able to evaluate the impact of a substantial, expensive health policy change. In a collaboration by the state and researchers, Medicaid coverage was randomly extended to some low-income adults and not to others, and researchers have been tracking the consequences ever since. Rigorous evaluations of health policy are exceedingly rare. The United States spends a tremendous amount on health care, but very little of it learning which health policies work and which don’t. In fact, less than 0.1 percent of total spending on American health care is devoted to evaluating them. As a result, there’s a lot less solid evidence to inform decision making on programs like Medicaid or Medicare than you might think. There is a similar uncertainty over common medical treatments: Hundreds of thousands of clinical trials are conducted each year, yet half of treatments used in clinical practice lack sound evidence. As bad as this sounds, the evidence base for health policy is even thinner. A law signed this year, the Foundations for Evidence-Based Policymaking Act, could help. Intended to improve the collection of data about government programs, and the ability to access it, the law also requires agencies to develop a way to evaluate these and other programs. Evaluations of health policy have rarely been as rigorous as clinical trials. A small minority of policy evaluations have had randomized designs, which are widely regarded as the gold standard of evidence and commonplace in clinical science. Nearly 80 percent of studies of medical interventions are randomized trials, but only 18 percent of studies of U.S. health care policy are. Because randomized health policy studies are so rare, those that do occur are influential. The RAND health insurance experiment is the classic example. This 1970s experiment randomly assigned families to different levels of health care cost sharing. It found that those responsible for more of the cost of care use far less of it — and with no short-term adverse health outcomes (except for the poorest families with relatively sicker members). The results have influenced health care insurance design for decades. In large part, you can thank (or curse) this randomized study and its interpretation for your health care deductible and co-payments. More recently, the study based on random access to Oregon’s Medicaid program has been influential in the debate over Medicaid expansion. A state lottery — which provided the opportunity for Medicaid coverage to low-income adults — offered rich material for researchers. The findings that Medicaid increases access to care, diminishes financial hardship and reduces rates of depression have provided justification for program expansion. But its lack of statistically significant findings of improvements in other health outcomes has been pointed to by some as evidence that Medicaid is ineffective. Although there are other examples of randomized studies in health policy, the vast majority have far less rigorous designs. Some of them are sponsored by the Center for Medicare and Medicaid Innovation, created by the Affordable Care Act. It has spent about $1 billion a year on dozens of programs that pay for Medicare and Medicaid services in new ways intended to enhance quality and reduce spending. Most of the innovation center’s pilots lack randomized designs, for which it has been criticized. Also potentially problematic: Most of its programs rely on voluntary participation by health care organizations. There might be crucial differences between those that opt in and those that don’t. Mandatory participation poses its own set of challenges. “If you force a hospital to join a new program, but not its competitor down the street, you might put the hospital at an unfair financial disadvantage,” said Nicholas Bagley, a University of Michigan health law professor. Also, testing voluntary participation makes sense if the program is never intended to be mandatory in the first place. In considering a mandatory program, you also have to be mindful of politics. “There will always be winners and losers,” said Darshak Sanghavi, a former senior official for the Center for Medicare and Medicaid Innovation. “If losers are forced to remain in a program, that could cause a political backlash that might blow the whole thing up.” Randomization can also be challenging; it can be complex and hard to maintain. “A program with desirable features for evaluation, like randomization, that falls apart could be less valuable than one that was designed more realistically from the start,” he said. Problems can also plague rollouts that are voluntary and not randomized. Programs showing promise suffer from diminishing participation as health care organizations drop out. The innovation center’s pioneer accountable care organization program offered health care organizations the opportunity to earn bonuses in exchange for accepting some financial risk, provided they meet a set of quality targets. It started with 32 participants in 2012. Although studies showed it reduced spending and at least maintained, if not improved, quality, only nine remained by 2016 when the program ended. Some of the largest innovation center programs — involving thousands of providers — bundle payments across services for some common treatments (like knee and hip replacements) instead of paying separately for each one. More efficient providers that can deliver the care for less than that price can keep some of the difference as profit. Those that can’t lose money. Of six bundled payment programs, only one included random assignment. Beginning in April 2016, Medicare randomly assigned 75 markets to be subject to bundled payments for knee and hip replacements, and 121 markets to business as usual. But the innovation center didn’t maintain the design, announcing in November 2017 that hospitals could leave it. This will greatly limit what can be learned from the program. Just as in clinical care, there are examples of incorrect thinking based on low-rigor studies that more rigorous ones later overturn. For example, many low-quality studies suggest that wellness programs reduce employers’ health care costs as they improve health outcomes. But when the programs have been subject to randomized controlled trials, none of these findings hold up. Hospital cost shifting — the idea that shortfalls from Medicare or Medicaid cause hospitals to charge higher prices to private insurers — can also seem commonplace from studies without rigorous designs. But when subject to more careful evaluation, the phenomenon is almost never observed. An apparent preference for ignorance is not unique to health care. Policies across governments at all levels are routinely put in without plans to find out if they work — or how to unwind them if they don’t, or how to build on them if they do. A 2017 Government Accountability Office report found that the vast majority of managers of federal programs were not aware of any recent evaluation of the programs they oversaw. In most cases, none had been done. In others, none had been done in the past five years. It’s hard to rid ourselves of ideas that are little more than wishful thinking or to end policies that don’t work. The first step would be to do more rigorous policy evaluations. The next would be to heed them. Check the chip guidelines carefully before exploring the CHIP programs, this will help you to find best plans for your child.  As telehealth benefits for minor injuries or illnesses continue to become a staple of strong company benefits packages, there’s one other area of care that deserves to go digital: mental health services.

Obstacles to Mental Health CareTelemedicine is a natural fit for the challenges of addressing mental health. Consider everything an employee needs to do to receive care for a mental health issue, something roughly 1 in 5 adults struggles with each year:

How Telemedicine Services Can HelpEnter telemedicine, a confidential and convenient route to care. Already, about 58% of major hospitals in the U.S. have already brought in virtual health to support mental health services. But it’s not only embraced by brick-and-mortar health systems: Telehealth companies like LiveHealth Online, part of the Anthem Blue Cross Blue Shield network, also offer video-based mental health care that costs about as much as a regular copay for some policyholders. There are many reasons why these emerging digital solutions can be so attractive for employees in need of mental health support:

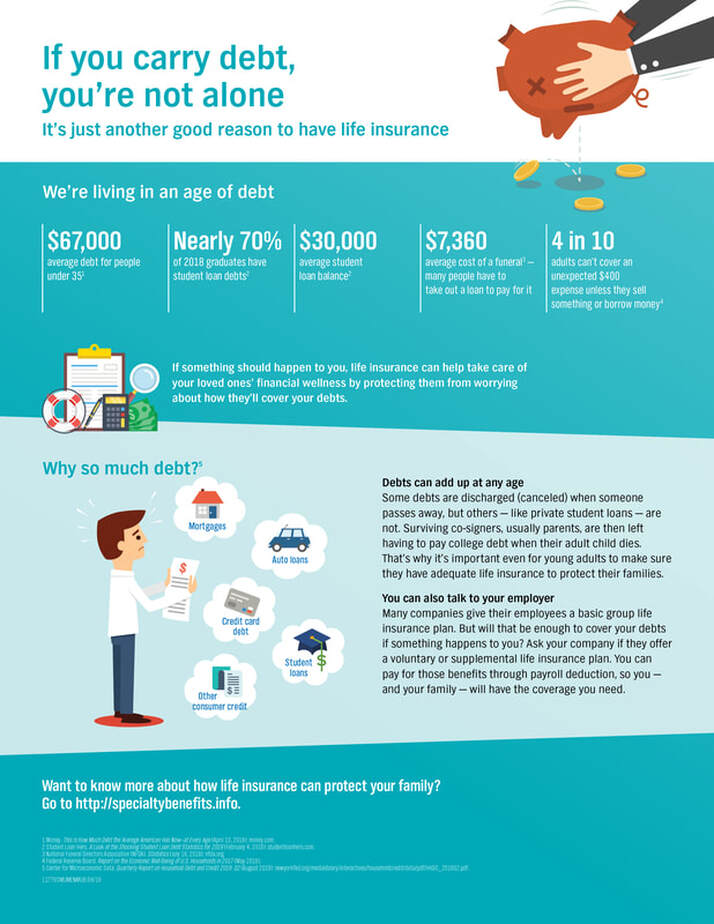

Is Telehealth Right for Everybody? These benefits make a compelling case for offering telemedicine, but keep in mind that some employees may still prefer seeing a professional in person. That’s why it’s important to enhance, rather than replace, mental health benefits with telemedicine solutions. The goal should be to break down barriers wherever they appear so that employees can get the care they need. With so many U.S. workers struggling in silence, it’s important to give them opportunities to speak to someone who can help. Whether they do so over a phone or in person — or maybe both — is up to them. They just need to know that someone, somewhere, is there to listen. Stay up to date on the latest health care regulations and trends for your small business health insurance plans.  Many employees depend on employer-sponsored benefits to help them achieve their financial security and wellness goals. An often under-appreciated benefit is group life insurance – especially with younger employees who are dealing with large amounts of debt in their lives. According to Money magazine, the average debt for a person under age 35 is $67,000. Life insurance can safeguard other family members against the most common types of debt including mortgage, student loans and can help with funeral expenses. The entire month of September is devoted to Life Insurance Awareness and it is a perfect time for employers to educate and encourage their employees to enroll in this important benefit. Share this infographic about the importance of life insurance with your employees. You also might also enjoy this article on the subject – The True Value of Life Insurance in Overall Financial Wellness by Greg Poulakos, Anthem’s President of Disability, Absence, Life & Supplemental Health business. Contact your insurance broker, benefits consultant or insurance carrier for more ways life insurance and business health insurance can protect the financial health of your employees and business.   The following is an example of the people whom our organization strives to help every day.

Ms. Santos got off the bus after working a 14-hour day as a housekeeper, when she noticed an unbearable pain in her abdomen. She continued to walk toward home, thinking it will go away soon. That evening, she noticed the pain worsening, decided to make some herbal tea in hopes of alleviating her symptoms, and then went to sleep. The next day, the pain persisted when she woke up. The idea of going to a doctor passed through her mind but was quickly overshadowed with the fact that as a single mother providing for her two children, she needs the income from her 14-hour workday to meet her family’s basic expenses. She doesn’t have a designated primary care provider, and she was afraid of not being able to communicate with a provider who did not understand her cultural background and values. After all, she hasn’t seen a health care provider in the two decades she’s been in the United States. As she made the decision to not seek care, she walked out of the house and into another 14-hour, labor-intensive workday with intensifying abdominal pains. Cultural competence in health care is not merely a box to check. Rather, it is a foundational element of providing high-quality health care and a bedrock for meeting the needs of an increasingly diverse population of patients. Cultural competence becomes effective when those working for health care providers and health systems—from the sanitation staff to the chief medical officer—systematically consider how to integrate it into their approach in delivering care and their interactions with patients. This understanding is nothing new. In research published in Health Affairs in 2005, the authors—from Harvard Medical School, Beth Israel Deaconess Medical Center, and Weill Medical College of Cornell University—wrote that cultural competence was “evolving from a marginal to a mainstream health care policy issue and as a potential strategy to improve quality and address disparities,” following their interviews with 37 experts in cultural competence from managed care, government, and academia. Cultural competence, they said, was emerging for three reasons:

More recent research published in PLOS ONE in 2015 focused on end-of-life conversations. Here, researchers from Stanford University School of Medicine found that doctors often struggled to talk to patients of a different ethnicity. A Personal Experience The health care system can be daunting for anyone, let alone for people who may lack the appropriate resources to navigate its complexities. From providers to paperwork, a simple trip to the doctor’s office can be confusing and intimidating for many patients. For those for whom language or cultural barriers exist, this presents even more layers of complexity and anxiety, creating systemic barriers to care for this population. Throughout my career, I’ve set out to change the system at a community level to better meet the needs of those patients. As an executive director of a public mental health integration program within the New York City Department of Health and Mental Hygiene, I work to recruit, train, and deploy behavioral health clinicians across New York City—and ultimately help high-risk, vulnerable populations gain greater access to culturally competent care. While there are tremendous challenges, there’s a very clear need to create new pathways and strategize on how we develop tomorrow’s clinical workforce, not just to address current or future shortages, but to do so with cultural humility in mind. We’re working to take cultural understanding to the next level, appreciating cultural differences in a way that helps us diversify our health care workforce and really connect with the people we serve. As president of the Academy of Medical & Public Health Services, a public health not-for-profit organization in Brooklyn, New York, I work to integrate the mainstream health system with the community-based social support system through a workforce of community health workers who help coordinate care for high-risk, vulnerable immigrants, like Ms. Santos, who otherwise would not seek care. By having a workforce that hails from the same community as the people we serve, who look like that community, speak the same language, and understand its cultural values, we increase access to—and quality of—care simultaneously. The United Health Foundation's Diverse Scholars Initiative Key to helping me on this path was my participation in the United Health Foundation’s Diverse Scholars Initiative. As part of the initiative, I received a scholarship from the Asian & Pacific Islander American Scholars to help me attend New York University (NYU) in a joint-degree neuroscience and public administration program with a specialization in health law and finance, through the NYU College of Arts and Sciences’ Center for Neural Science and the NYU Wagner Graduate School of Public Service. Through participation in the Diverse Scholars Initiative annual forum, I learned about complex health policy issues at a national level, which helped me to better understand the intricacies of our health care system in the United States and at the local level. In 2019 the Diverse Scholars Initiative provided assistance for nearly 230 scholars across 40 states. Since the United Health Foundation launched the initiative in 2007, it has provided more than $20 million in assistance to students and funded nearly 2,600 scholarships to undergraduate and graduate students who are pursuing careers in primary care and who demonstrate a commitment to working in underserved communities. One of the foundation’s core missions is to build healthier communities by helping to modernize and diversify the health care workforce to meet the needs of people from all backgrounds. That means investing in people, technology, and programs to keep up with the rapid pace of change in the industry. Continuing to integrate cultural competency into the health care system requires an all-hands-on-deck approach. All stakeholders—from hospitals and health systems, to physician practices, to health insurers, to government agencies, to educational institutions, and beyond—must be willing to recognize the needs of people from all backgrounds and work to prioritize meeting those needs so as to optimize care. After all, the best care we can give someone is informed by who they are. Check the chip application pa carefully before exploring the CHIP programs, this will help you to find best plans for your child.  By 2017, Medicaid expansion had provided health coverage to more than 17 million low-income adults in 32 states and helped lower the overall uninsured rate in the United States to 8.8 percent. But critics have long looked for highly misleading ways to undermine the program, such as portraying improper payments and enrollment errors as Medicaid beneficiary fraud or claiming Medicaid expansion has fueled the opioid crisis. The latest is an attempt to argue that the people enrolling in Medicaid do not qualify.

In a recent Wall Street Journal (WSJ) commentary entitled “Obamacare’s Medicaid Deception,” authors Brian Blase and Arron Yelowitz draw inaccurate conclusions about the Affordable Care Act’s (ACA) expansion of Medicaid to low-income adults. The authors wrongly assert that “most people who gained coverage have enrolled in Medicaid regardless of income.” The commentary is based on a National Bureau of Economic Research (NBER) working paper using income data and coverage source reported by individuals in the Census Bureau’s Annual Community Survey (ACS). But the NBER study, co-authored by Yelowitz, does not make adjustments to the ACS data to simulate the complex construct of how income and household size are actually counted and verified for adults in Medicaid. Nor is it based on actual administrative enrollment data. To explain his error, it would be most appropriate to discuss how the ACS calculates income, since the primary but unproven conclusion of the commentary is that a large share of individuals with Medicaid coverage are not income-eligible. In fact, there are many reasons ACS survey income data would not align with the way income is counted in Medicaid. First, Medicaid eligibility is based on taxable – not gross – income. Second, certain types of income, such as Supplemental Security Income for low-income, disabled adults, child support, and Veterans benefits are not included in household income when determining eligibility for Medicaid expansion adults. Third, household size for Medicaid is based on the number of individuals in the tax-filing unit for tax-filers while only parents and children are counted in non-tax filing households. The ACS household requests information for everyone in the household, including non-married partners, in-laws, roommates, and other individuals who should not be counted in determining the household size or income for Medicaid. This brief from the State Health Access Data Assistance Center (SHADAC), although focused on estimating Medicaid eligibility for the adult population pre-ACA, illustrates how results differ when adjusting Census data appropriately for household size and income. The study found that relying on unadjusted data underestimated the number of adults with income at or below 138 percent of the federal poverty level (FPL) by 16 million, or 8.9 percent, in 2010. Importantly, Medicaid eligibility is not determined based on self-reported income. All income must be verified through trusted electronic sources when possible, or through documentation provided by the enrollees. Additionally, Medicaid eligibility is based on current monthly income – not total income in the past 12 months - as income volatility is significant among low-income individuals. According to this Health Affairs study, more than one-third of individuals with income below 200 percent FPL shift in or out of Medicaid eligibility in a six-month period and, within a year, 50 percent will. Individuals who experienced a decrease in income as a result of job change or reduction in hours may qualify for Medicaid mid-year but appear to be over-income for the year overall. Another crucial point to understand is that income thresholds can vary by population within Medicaid. Pregnant women, individuals with disabilities, and those needing long-term services and supports may qualify for Medicaid at higher incomes. For example, according to data from the Kaiser Family Foundation, the median eligibility level for pregnant women is 205 percent of the federal poverty level (FPL) and the median income for disabled individuals to “buy-in” to Medicaid is 256 percent FPL, both well above the Medicaid adult expansion threshold of 138 percent FPL. The NBER study attempts to test its results against these potential alternative pathways, but it does not provide a sufficient explanation to fully understand how it conducted these sensitivity tests. And while the sensitivity analysis appears to substantially change their results, the authors still focus on the unadjusted numbers. As a result, the commentary’s conclusion that “virtually all of the increase in participation for income-ineligible adults is coming from those with no obvious path to qualify for Medicaid” is completely unsubstantiated. The authors try to buttress their unfounded conclusion by grossly misrepresenting the results of a legislative Medicaid audit in Louisiana with their statement that “82 percent of expansion enrollees were ineligible at some point during the year they were enrolled.” The fact is that the Louisiana audit first identified fewer than 20,000 enrollees – less than 4 percent of the estimated 500,000 expansion enrollees – whose income appeared to exceed the Medicaid eligibility level at some point during their enrollment. From that group, the audit pulled a targeted sample of just 100 individuals with the highest wage amounts during a study period over 21 months and determined that 82 people were ineligible for coverage for some period of time (without taking into consideration the relevant rules and actual data sources that were appropriately used to calculate eligibility initially). In no way does the audit conclude that 82 percent of all expansion enrollees were ineligible at some point during their enrollment as authors incorrectly declare. The bottom line is this – the NBER working paper used as the basis for the WSJ commentary is relying on unadjusted self-reported survey data as a proxy for actual Medicaid income eligibility and enrollment. It cannot and should not be construed as an audit of improper enrollment. The ACS is a reliable data source but should not be used to draw misleading conclusions about income eligibility and enrollment in Medicaid as the authors do. Instead, researchers should follow best practices in using public data – such as the State Health Access Data Assistance Center and the Urban Institute do -- to simulate how eligibility is determined in Medicaid. If you want to know more about the business health insurance then please send your queries by dropping a comment below.  The choices are numerous and confusing. Whether you’re looking for yourself or your parents, here is some guidance.

We were so confused. My wife’s mother was going through medical issues that could potentially have left her needing long-term care. But we had never taken a hard look at our options if that happened. She lives 2,000 miles away, and we all had to start thinking about what the next steps would be if things did not go well with her. And we had no idea where to start. We didn’t even have the vocabulary: What’s the difference between assisted living and a nursing home? So we began to study, and visited an assisted living facility near our home to get a sense of our options. In our ignorance, we were like a lot of other people. Few of us are prepared, or even want to think about, the options for our parents — or, especially, for ourselves. “Even the most sophisticated people have no idea what these things mean,” said Daniel Reingold, president and chief executive of RiverSpring Health in New York. And yet, he noted, while aging happens gradually, the need for long-term care can arise suddenly. “Frequently, the decision-making process comes in a crisis,” like when a parent falls or begins to wander the neighborhood, he said. It’s easy to see why people don’t plan ahead. Infirmity and mortality are frightening. Ruth Katz, senior vice president of public policy/advocacy at Leading Age, an industry group representing nonprofit senior service providers, said, “People don’t like, in the prime of their lives, to think about the possibility that you’re going to need help doing very personal things,” including going to the bathroom and getting out of bed. Research from the Department of Health and Human Services suggests that more than half of Americans now turning 65 will need long-term care and services, and one in seven adults will have some kind of disability for more than five years. Infirmity, then, is predictable, and is, at least, something we should plan for. But then there’s the cost. “People think they have an issue paying for a college education — wait ’til you see how much long-term care costs,” said Nicholas Castle, a professor in the School of Public Health at West Virginia University. The Health and Human Services report says someone turning 65 today will pay, on average, $138,000 for their long-term care, with families paying about half the cost and the rest picked up by public programs and insurance. The average cost of living in a private room in a nursing home is more than $90,000 a year, which beats even Sarah Lawrence. This, then, is an introduction to the basics of long-term care, to help you start your own search more informed — whether you are planning for the care of a parent or yourself. STAYING HOME When trouble strikes, what most people want is to stay at home as long as possible, with assistance from family or paid assistance that can include a home care aide or nurse. That option can even include retrofitting the home with features like ramps and grab bars. (Health insurance and Medicare might pay for some of those services, for a certain amount of time.) INDEPENDENT LIVING Some people decide to move to independent living complexes, which can offer a sense of community and activities while letting somebody else take care of some of the irritations like lawn care, housekeeping and cooking meals. ASSISTED LIVING For those who find themselves unable to live independently, however, and need help with activities of daily living — which can include help with getting dressed, going to the toilet and sorting medications — this is an option. It can have much of the look and sensibility of independent living but with a higher level of care and monitoring. Many of these facilities also offer what’s known as memory care for people with cognitive impairment like Alzheimers and other forms of dementia. NURSING HOMES These facilities provide round the clock care for people with more serious health conditions. Many people resist the idea of nursing home care, though the facilities are regulated under federal law, unlike assisted living facilities, which are regulated under a patchwork of state laws and vary widely. Nursing homes qualify for a substantial degree of coverage under Medicaid, which generally kicks in after other assets are depleted. For many people, nursing homes can be the best option, Ms. Katz said. “Friends will say to me, ‘I think it’s time for my mom to move into someplace where she will get some help — I don’t think she needs to go into a nursing home. She only needs assisted living.’ I want to ask, ‘What do you mean — and what do you think you mean?’” Some facilities known as continuing care retirement communities offer a blended approach, which allows residents to take on additional services as they need them. It can be an expensive option, with costs rising as the level of care rises. Professor Castle of West Virginia University recommends careful shopping, with visits to facilities and an eye out for hidden costs. “It’s a bit more complicated than buying a car,” he said. And, he added, a family might need care quickly, “but the correct care might not be the correct care for the next two or three years.” Then there is the question of whether the kind of care that’s needed is even available where you live, especially in rural areas where options can be few. “You can have some of the best nursing homes around in your location, and it doesn’t mean they’re going to have a bed,” he said. When planning for parents, it’s important to ask what they want. My mother-in-law told us that she had worked as a nurse in a nursing home, years ago, and the experience was a sad one. “I don’t want to be in a place like that,” she said, though she acknowledged that many facilities have most likely upgraded since then. She did not want to move out of her home unless she absolutely had to. Ultimately, she was able to get by with some help at home for a number of weeks until she had fully recovered. Still, the research we had done was helpful; we felt that we could confront the future with a little more confidence the next time these questions came up. If you want to know more about the small business health insurance then please send your queries by dropping a comment below.  Health care, so far perhaps the biggest issue in the Democratic primary, is also the most complicated issue facing government and the public. Unfortunately the debate is filled with persistent misconceptions, from the role insurance company profits play in health care costs to who is actually paying for workers’ health coverage.

Clarifying four fundamental health care fallacies could make it easier for voters to square some of the Democratic proposals — and their critiques — with reality: Fallacy No. 1: Employers pay for employees’ health insurance. Employers write checks that cover most health insurance premiums for employees and their dependents. But as the Princeton health economist Uwe Reinhardt once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself. With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary. The fallacy is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one though not the only reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the belief that employees don’t pay for their own health insurance is widespread. One reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades. Another reason is that employers want Americans to believe that they pay for their workers’ health insurance. Still another reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals. They all want you to believe companies are being magnanimous in giving you insurance. Who else benefits from the belief in this fallacy? Opponents of national health insurance. Fallacy No. 2: Medicare for All is unaffordable. The key to evaluating the cost of Medicare for All is to distinguish between increasing spending on health care and shifting expenditures from private insurance to the federal government. True, Medicare for All would increase federal health care spending. But that is not the same as increasing total health care spending, which was over $3.5 trillion last year. Instead, Medicare for All would move money from one column (private health insurance spending) to another (federal health spending); it does not automatically increase total costs. A recent study by the Mercatus Center at George Mason University — a free-market center generally hostile to government programs — estimates that for the 10 years between 2022 and 2031 the total national health costs for Senator Bernie Sanders’s Medicare for All plan would actually be $50.1 trillion. That would be $2 trillion less than if we let the system operate as it currently does. However, Mercatus researchers doubt that the Sanders’s plan would ultimately save trillions because they believe Congress would have to increase Medicare rates paid to hospitals and physicians to get the legislation enacted. They may be right — or wrong. But that is a different argument — a prediction about the politics of enacting laws — than that Medicare for All would inherently increase total health care spending. We have our doubts about Medicare for All. But unaffordability is not a reason to oppose it. Whether it’s our current arrangement or a future Medicare for All, the per capita cost of our health care system already far exceeds that of any other industrialized country — including those with single-payer systems. When you hear a health care price tag in the trillions, know that the existing system has already brought us there. Fallacy No. 3: Insurance companies’ profits drive health care costs. In the second Democratic presidential debate, Senator Bernie Sanders declared that the health care industry makes $100 billion in profits. He once railed against the insurance company Anthem for denying a claim while noting that it reported “fourth-quarter profits for 2017 had increased by 234 percent to $1.2 billion.” Many Americans believe that profits have no place in health care. They see for-profit health insurance, like buying and selling kidneys and livers for transplantation, as what the Nobel Prize winner Alvin Roth termed a “repugnant industry” — something that should not be exchanged in the market. That is an important moral stand, but it makes no difference to the claim that eliminating for-profit insurers will reduce high health care costs. The fact is, we could eliminate those profits and it would hardly matter to the cost of health care. You would not notice it in your premiums. For the eight largest for-profit health insurance companies, in 2016, their cumulative revenue amounted to nearly $452.2 billion and profits were $22.1 billion, for a profit margin of about 5 percent. By contrast, technology companies, banks and major drug companies generally make more than 20 percent profit. True, $22.1 billion is a lot of money — but it is 0.6 percent of health spending. And last year alone health care costs increased over $130 billion — six times insurance company profits. Health care spending would not be significantly cheaper if all insurance companies’ profits were zero. There are far more savings to be had in other efforts — by cutting unnecessary patient services, for example, or by making physicians and hospitals more efficient — to deliver the same care at a lower cost. Fallacy No. 4: Price transparency can bring down health care costs.“Hospitals will be required to publish prices that reflect what people pay for services,” said President Trump when he signed his executive order on health care price transparency. “Prices will come down by numbers that you wouldn’t believe. The cost of health care will go way, way down.” There is no doubt that prices for medical procedures can range widely even within the same city or state. For instance, M.R.I.s of the spine can vary threefold in Massachusetts and mammograms fivefold in San Francisco. Conservatives argue that informing patients of prices for tests and treatments will induce them to shop for lower-cost services, saving them, insurers and the country money. In theory, the beauty of price transparency is that neither the government nor insurers impose cost controls; the invisible hand of the market does it all. Yet demonstrations of price transparency have been tried many times in many places, and in reality, it has not reduced the cost of care. One recent study by Harvard Medical School researchers involved hundreds of thousands of employees and used a website telling them what they would pay out-of-pocket if they chose particular physicians and hospitals. The result: no savings. A follow-up study using another set of employers and another price transparency tool found the same result: no savings. Since 2007, New Hampshire has had a state website, N.H. Health Cost, that allows patients to select a medical procedure, insurer and ZIP code and then get a list of prices for the procedure from various providers. The most promising study of N.H. Health Cost suggests a few million dollars in savings per year. That works out to be about $5 per New Hampshire resident. The fact is, price transparency will not make health care costs “go way, way down.” Health insurance insulates the patient from price. Over 80 percent of the cost of medical care is paid by private and public insurance. Patients have little incentive to seek out the cheapest provider. When pricing websites exist, few patients use them. Even in the most favorable studies, when offered a price transparency tool, only 12 percent of patients took advantage of it; usually it’s less than 4 percent of patients. Furthermore, price considerations are useful for choosing only about 40 percent of procedures — routine services like colonoscopies, M.R.I. scans and laboratory tests. Most of the expensive services — think heart catheterizations, cancer chemotherapy and organ transplants — are not the kind of thing you decide based on price. Finally, in health care, Americans usually put relationships ahead of money. Once patients find a physician they trust and a hospital they like, they tend to stick with them even if there is a lower-cost alternative nearby. American health care is complex and any simplistic solution is likely to be based on a fallacy. But that doesn’t mean there is nothing we can do. There are solutions — they just don’t make for bumper sticker phrases like Medicare for All or Eliminate For-Profit Insurers or Price Transparency. Explore chip health insurance pa and get the best plans for your children, if you want to know more details then please send your queries in the comment section.  With M&A activity for life insurers or blocks of in-force business poised for a possible spike, acquirers of life businesses should consider factors that are peculiar to, or disproportionately affect, the life and annuity sector relative to other types of insurers such as property-casualty (p&c).

Such features specific to life companies include the following, which require a dedicated focus on due diligence and may also require appropriate tailoring of representations and warranties or other provisions in the purchase contract:

It can be expected that compliance with these rules for new business will be a key focus of New York and other state insurance regulators going forward. Acquirers will want to make sure they understand the reach of any such new requirements and the resulting compliance implications for their target.

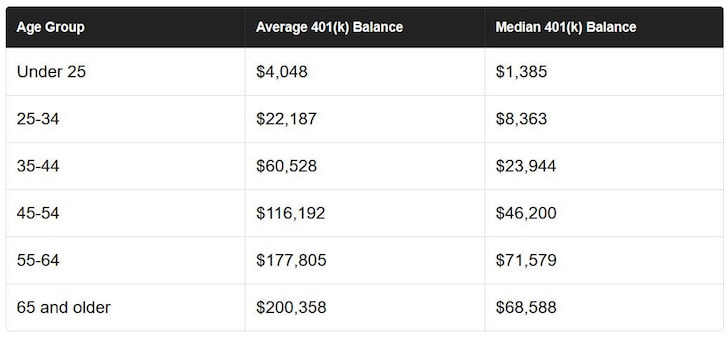

An acquirer should consider all these developments carefully in the context of a particular insurance target, not only from a valuation standpoint but also for purposes of representations and warranties in the purchase agreement such as those relating to actuarial reserving, reinsurance, investments, capital adequacy and regulatory and other compliance. If you want to know more about the pa health insurance companies then please send your queries by dropping a comment below.  You likely won’t be able to live off your 401(k) alone in retirement, but you should be able to combine your 401(k) with alternative savings, other passive investments, and Social Security to live a financially free life when the time comes to withdraw at the age of 59.5. Most Americans don’t have pensions. The reality is that the median account balance in the U.S. is only around $72,000 for 55-64 year olds in 2019 according to Vanguard, one of the largest 401k managers. The average 401k balance for 55-64 year olds is roughly $178,000. But the average is screwed up to due the super wealthy. Even with $178,000 in your 401k at retirement age, you aren’t going to be living it up for the next 20 – 30 years without alternative sources of income.  According to data from Fidelity, here’s the average 401k breakdown by age in 2018: