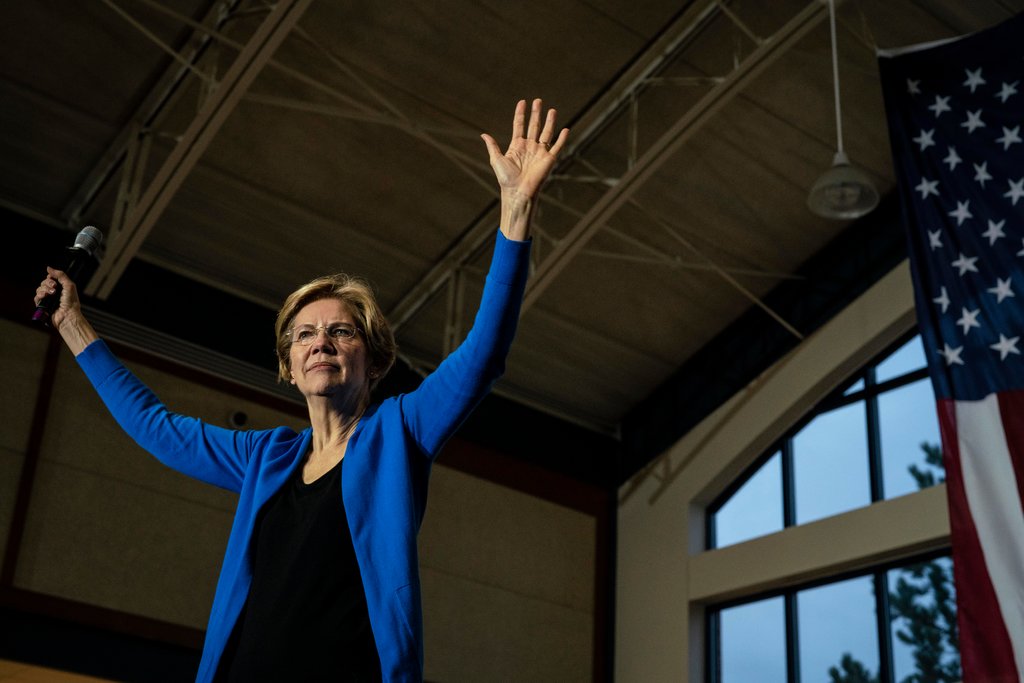

WASHINGTON — Senator Elizabeth Warren vowed on Friday to pass major health care legislation in her first 100 days as president, unveiling a new, detailed plan to significantly expand public health insurance coverage as a first step, and promising to pass a “Medicare for all” system by the end of her third year in office that would cover all Americans.

The initial bill she would seek to pass if elected would be a step short of the broader Medicare for all plan she has championed. But it would substantially expand the reach and generosity of public health insurance, creating a government plan that would offer free coverage to all American children and people earning less than double the federal poverty rate, or about $50,000 for a family of four, and that could be purchased by other Americans who want it. Ms. Warren has long endorsed a Medicare for all bill sponsored by one of her rivals for the Democratic nomination, Senator Bernie Sanders of Vermont. But until now, she has not specified how quickly she would move to enact a health care plan. Friday’s proposal amounts to a detailed road map for eventually establishing Medicare for all, a single government-run health insurance program under which private coverage would be eliminated. That goal — a wholesale transformation of how Americans receive health insurance — is a big political gamble, particularly given that many of them would have to give up the coverage they get through their employers. Ms. Warren’s proposal for Medicare for all would require an estimated $20.5 trillion in new federal spending over a decade, according to a financing plan she released two weeks ago. To provide funding for it, she would impose new taxes on businesses and the richest Americans. But under the plan she presented on Friday, she would not seek passage of a single-payer system early in her presidency. The proposal would instead move people into that system gradually — in a way she hopes would build public support for full-fledged Medicare for all — while temporarily preserving the employer-based insurance system that covers most working-age adults today. “I believe the next president must do everything she can within one presidential term to complete the transition to Medicare for all,” Ms. Warren, of Massachusetts, wrote in her plan. “My plan will reduce the financial and political power of the insurance companies — as well as their ability to frighten the American people — by implementing reforms immediately and demonstrating at each phase that true Medicare for all coverage is better than their private options. I believe this approach gives us our best chance to succeed.” Though the details differ, Ms. Warren’s transition plan shares many features with health care proposals from her more moderate rivals for the nomination, including Joseph R. Biden Jr., the former vice president, and Pete Buttigieg, the mayor of South Bend, Ind. For example, it would allow higher-income adults to voluntarily sign up for a new public plan. Ms. Warren’s proposal, however, would make the optional government plan more generous than those proposed by her rivals, and would allow more Americans to get it free. It would also let anyone over 50 buy Medicare coverage, with more benefits than the program offers now. With her interim plan, Ms. Warren is attempting to offer something attractive to both sides of the Democratic health care debate: preserving her commitment to the single-payer vision that energizes voters on the left, while offering a less disruptive set of proposals in the short term to those who may be reluctant to give up their existing coverage. But her choice to put off seeking passage of a full-scale Medicare for all plan until as late as her third year in office could draw criticism from liberals eager to put in place a single-payer system as quickly as possible. “Now, some people say we should delay that fight for a few more years,” Mr. Sanders said on Friday as he discussed Medicare for all and the opponents who would try to stop it. “I don’t think so. We’re ready to take them on right now, and we’re going to take them on on Day 1.” And on Twitter, he offered his own pledge about the beginning of his presidency: “In my first week as president, we will introduce Medicare for All legislation.” Representative Pramila Jayapal, Democrat of Washington, who has introduced Medicare for all legislation in the House, praised Ms. Warren’s plan as “one smart approach” that “gets us to Medicare for all that covers everyone with comprehensive care in four years.” Ms. Warren’s plan reflects a sense of pragmatism about the politics and logistics of passing a major health bill through a closely divided Congress. Ms. Warren said she would pass the transition plan using special procedures that would require only a simple majority in the Senate, rather than the 60 votes needed to overcome a filibuster. But she would still rely on Democrats winning control of the Senate, where Republicans currently hold a slim majority. And she is laying out ambitious details for getting to a single-payer system even as voter support for the idea is narrowing; polls suggest substantially more Americans prefer the “public option” type of plans that Mr. Biden and Mr. Buttigieg have proposed. Kate Bedingfield, a deputy campaign manager for Mr. Biden, said Ms. Warren was “trying to muddy the waters even further” after “having discovered how problematic her embrace of Medicare for all has become.” “What started out as ‘mathematical gymnastics’ have been replaced by a full program of flips and twists covering every element of her plan,” she said, adding that the transition plan “doesn’t change the reality that Medicare for all will deny Americans the right to choose their insurance by eliminating employer-sponsored insurance.” Passing a health bill could crowd out other legislative priorities. President Trump’s efforts to repeal and replace major parts of the Affordable Care Act in 2017 stretched well beyond his first 100 days and ultimately failed. And given the unpredictable nature of politics, a pledge to pass comprehensive Medicare for all legislation by the end of 2023 represents a somewhat distant goal. “I think that it’s really unnecessary and potentially dangerous to try to split up something like Medicare for all into multiple bills,” said Dr. Adam Gaffney, the president of Physicians for a National Health Program, a group of doctors that supports a single-payer health care system. But he said he was pleased Ms. Warren was still advocating Medicare for all. When Ms. Warren laid out her plan to finance a Medicare for all system earlier this month, she said that she would not increase taxes on middle-class families by “one penny.” Among other revenue sources, Ms. Warren would require employers to pay an amount similar to what they are currently spending on their employees’ health care, and she would raise taxes on the richest Americans, including by steepening her proposed wealth tax for billionaires. Her transition plan did not come with its own detailed financing proposal, but it said the interim program would cost the federal government less than an eventual Medicare for all system and would be funded using some mix of the revenue sources she has already identified. The plan also spells out a long list of administrative actions Ms. Warren would take to change the health care system, even if Democrats do not retake the Senate. She would roll back Trump administration regulations that have weakened the Affordable Care Act and broaden benefits in the existing Medicare program. She would also use executive authority to allow new generic versions of expensive drugs — such as insulins taken by patients with diabetes, treatments for hepatitis C and the overdose reversal drug Naloxone — in an effort to lower their prices. As Ms. Warren has established herself as a leading candidate for the Democratic nomination, her opponents have frequently attacked her over health care, a top issue in the primary. For much of the fall, her refusal to say whether she would raise taxes on the middle class provided an opening for some of her rivals to paint her as cagey on a key issue. Mr. Biden and Mr. Buttigieg have also argued their public option proposals are far more realistic than Ms. Warren’s plan for Medicare for all, emphasizing that her plan would take away people’s private health coverage. Lis Smith, a senior adviser for Mr. Buttigieg’s campaign, described Ms. Warren’s transition plan as “a transparently political attempt to paper over a very serious policy problem, which is that she wants to force 150 million people off their private insurance — whether they like it or not.” In the longer term, Ms. Warren’s embrace of Medicare for all would provide ammunition to Mr. Trump and his Republican allies if she became the Democratic nominee. Mr. Trump is already fond of equating Democratic approaches to health care with socialism. Ms. Warren is a co-sponsor of Mr. Sanders’s Medicare for all legislation, which includes a four-year transition. Though his legislation is best known for its endpoint, it includes a detailed plan for moving from the current health care system to that final goal. But Mr. Sanders’s transition relies on passing his entire plan. Ms. Warren, by contrast, has suggested splitting the process in two: starting with the transition plan and only later passing a full Medicare for all bill. And Mr. Sanders, unlike Ms. Warren, has declined to specify a detailed financing plan for his proposal. Do you want to know more details about health insurance please visit our service area.

1 Comment

The Democratic presidential candidates have been fighting over whether they should try to replace the health insurance system with a single government-run plan or create a government-run plan that Americans could choose to join.

But hidden outside this big debate is a harsh reality: If Democrats fail to retake control of the Senate, neither plan has much of a chance to become law. Elizabeth Warren, the Massachusetts senator, has allied herself with the “Medicare for all” wing of the party, saying she would propose a single-payer system. But on Friday, she released a second plan, a sort of steppingstone along the way that would create a more optional government program. Her transition plan is engineered to pass with only a majority of Senate votes, instead of the 60 usually needed to overcome a filibuster. But it also includes a long and detailed list of the things she would do if she couldn’t get Congress on board. That section of the report, which is likely to get less attention and draw less criticism than the rest, actually tells us a lot about what health care policy would probably be like in a Warren administration. President Trump was elected in part on a promise to transform the health care system. His efforts to repeal and replace the Affordable Care Act have been unsuccessful, as Republicans in the Senate are unable to agree on any one solution. But he has used his regulatory authority to make many of the changes he was unable to achieve through Congress, like expanding the availability of insurance plans that cover fewer benefits; reducing federal funding of Planned Parenthood; permitting states to establish work requirements for Medicaid benefits; and increasing the size of special accounts that workers can use to save money for health care expenses. He has also pursued other regulatory projects in health care, like his proposal, finalized on Friday, that would require hospitals to publicize the prices they have negotiated with insurance companies. He is allowing states to import drugs from Canada through regulatory power, and aiming to overhaul care for patients with renal disease. So what would Warren do? Her regulatory agenda can be divided into a few broad categories. But over all, she views executive authority in the same broad way that Trump does. Several of her proposals are likely to end up in court — as several of his have. Here are the big areas where she has regulatory ideas. Reverse Trump administration policiesOne big chunk of her plan would reverse some Obamacare regulations established by the Trump administration. She would return funding to Planned Parenthood and other reproductive health groups that also offer abortion services, for example. She would restore funding to publicize insurance options. She would eliminate new requirements on Medicaid beneficiaries, such as work requirements and premiums. And she would change rules to restrict the sale of so-called short-term health plans, which don’t follow all the Affordable Care Act’s rules. She would restore an Obama-administration policy that provided civil rights protections to transgender patients and women with a history of abortions, among other groups. Expand benefits in existing insurance programsShe would seek to offer subsidies to new groups of people to help them buy health insurance under Obamacare, including legal noncitizen immigrants and the families of people who can obtain coverage for only themselves through work. She would also seek to add a dental benefit to the Medicare program, by reinterpreting language in the statute that says dental care can be covered only if it is “medically necessary.” And she would change aspects of the Medicaid program, making it easier for states to offer coverage to more people, even if it will cost the government more. She would write new rules for a 2008 law that requires insurers to cover mental health care in the same way they cover care for physical ailments. The goal is to expand coverage for mental illness and substance abuse across different types of insurance. Lower drug pricesMs. Warren’s regulatory agenda is perhaps most aggressive in its efforts to limit drug prices. She proposes that the federal government employ never-before-used authority to rescind existing patents on medications that were developed with the help of government funding. She would also expand an infrequently used authority so that the government itself could manufacture certain drugs in public health emergencies. Among the drugs and devices she would target are insulin, EpiPens, antibiotics and medications for hepatitis C, H.I.V. and opioid overdoses. The list of policies above does not include everything that Ms. Warren has proposed. She’d also like to beef up antitrust enforcement in health care, for example. But it gives a sense of the breadth of things she would try to do in health care, even without Congress’s help. President Trump is far from alone in failing to enact his preferred health policies through legislation. Several presidents before him have struggled to pass major health overhauls. As Democrats head into another debate next week, the moderators may want to consider asking candidates what’s on their health care regulatory wish lists. The answer may be far more useful in predicting the shape of their policy agenda than the details of their legislative dreams. Step therapy, also known as “fail first,” is a process used by health insurers to control costs. It requires patients to try one or more medications specified by the insurance company, typically a generic or lower cost medicine, to treat a health condition.  The health care landscape is rapidly changing as employers, patients and health care providers look for ways to contain rising costs. But you don’t have to understand every part of this complex industry to bring about change.

Offering a health plan for your employees is a vote of confidence in that plan’s network, coverage and overall ability to improve your workforce’s access to affordable health care. Small business owners can further health care innovation by carefully assessing which plans will bring the most benefit — and the most value — to their employees. What Is Value-Based Care? For decades, the health care industry operated on a fee-for-service payment structure. If you received a service, your doctor or hospital was paid for that service, even if it wasn’t clinically necessary or didn’t end up improving your health. The value-based care model, on the other hand, aims to tie how patients pay for care to how effective that care is — in other words, how much value it brings. Value-based care has already been shown to reduce emergency department visits and inpatient hospitalizations, and it has led to improved preventive care and chronic disease management. What Role Do Employers Play? Nearly 50 percent of insured Americans get their insurance through their employers. The success of your business relies on your ability to attract and retain the best talent, which often means providing an appealing benefits package. But offering competitive benefits without straining your budget isn’t always easy. In order to properly assess health care costs, employers should understand what tools are available to control them. When choosing a health plan, look for one that includes the three pillars of value:

How Can Employers Find the Best Health Plan Solution? Many health plans tackle at least one of the pillars, but bringing them all together will give your business the best chance of delivering value in your employees’ health care. Anthem’s Cooperative Care pilot program, for example, helps employers in certain states control health care costs by rolling all three pillars into one plan. With the program, employees choose a primary care provider to act as their hub for medical services and use an ACO within a high-performance network. Specialists and other providers within the network are held accountable for the overall service they provide, with value-based payment models that reward providers for high-value/low-cost services and improved outcomes. Employees receive a health plan designed to furnish them with coordinated care, a deeper patient-provider relationship and better health outcomes with an emphasis on overall wellness. Anthem’s Cooperative Care program offers a special focus on the patient experience, with shorter wait times, lower costs and quality doctors all leading toward the goal of better health. Employers are poised to be a major force in the value-based care transformation happening across the health care industry. In choosing a plan for your employees, you’re making a claim about what you want the next health care innovation to look like — for your workforce and for yourself. Checkout the family health insurance lancaster pa plans and find the better options for your loved ones.  Cosmetic surgeries can become expensive quickly, and navigating insurance after these kinds of procedures can force patients to swim in murky waters. But with a little guidance, your employees can compare prices and find the best, most cost-effective provider.

Understanding Cosmetic Surgery Costs The cost of cosmetic, or aesthetic, surgery takes several factors into account. A deeply experienced surgeon might charge more, for example, as might one performing particularly complex procedures. Undergoing a cosmetic surgery in a large city could be cost more than having it done in the suburbs. And a hospital is generally the most expensive place to receive cosmetic procedures, but many cosmetic surgeries can take place — and cost less — at outpatient ambulatory surgical centers. Surgery that’s performed for purely aesthetic reasons generally isn’t covered by insurance. More likely to be covered are medically necessary procedures or reconstructive surgeries after trauma, for instance an accident, severe burns or cancer treatment. Insurers also routinely cover surgery meant to correct an issue present at birth. And you may find that insurance will cover part of a procedure that serves both a medical and an aesthetic purpose. For example, insurance may pick up a portion of a nose reshaping if the surgery made structural changes that improved breathing. For common procedures, you can receive an estimated price for the entire episode of care, including consultation, the actual procedure and any follow-up. The American Society of Plastic Surgeons (ASPS) provides averages for routine procedures to give you a basis for comparison. Rhinoplasty typically costs about $5,100, for example, while eyelid surgery averages around $3,000. Reconstructive surgery is more complex and may require a consultation to receive an accurate estimate. How to Control the Cost of Cosmetic Surgery First, employees should always check with their insurance to see if all or part of their procedure is covered. Get any approvals needed beforehand to help streamline the claims process. Employees can also take advantage of their health savings or flexible spending accounts to cover the costs of a surgery, as long as it’s medically necessary. They may need to obtain a letter of medical necessity to receive reimbursement or provide payment through their medical savings account, so planning ahead is key. The next step is to shop around. Encourage employees to call different doctors and ask for a cost estimate. They should get a detailed list of what is included in that cost and what additional expenses they may face, such as charges for ice packs, prescription medications or other needs. Before choosing a doctor, it’s a good idea to do some research and read online reviews. From there, employees should schedule consultation appointments with their top choices. Before getting any kind of cosmetic procedure done, they should feel confident in their doctor’s qualifications, how the surgery is done and the expected recovery time. The consultation is a chance to get any questions out of the way early on. Your employees should leave the meeting knowing the answers to the following questions, as recommended by the ASPS:

Most plastic and reconstructive surgeries are scheduled long in advance of the actual procedure, so your employees have the opportunity to take their time searching for the most competitive provider. It’s possible to have a cosmetic surgery done without draining your bank account — all it takes is a little planning. Explore private group health plan and get the best plan for business, if you want to know more details then please send your queries in the comment section.  Do you ever wonder why you’ve been hearing so much about the benefits of value-based care lately?

It’s not really new; it was just a long time evolving. In the late 1990s and early 2000s, researchers started seeking reasons for the overuse of health care services — often unnecessary health care services. Their findings? Misaligned incentives discouraged coordination and collaboration and encouraged a piecemeal approach to care, reports the Center for Health Care Strategies. Various organizations, including the Brookings Institution, the Institute for Healthcare Improvement (IHI) and the Patient-Centered Primary Care Collaborative, began looking for ways to align incentives to meet the Triple Aim, first articulated by IHI: “simultaneously improving the health of the population, enhancing the experience and outcomes of the patient, and reducing per capita cost of care.” The idea caught on: Reward quality and efficiency and penalize — or at least stop incentivizing — fragmented, volume-based care. The benefits of value-based care became clear, and so began the gradual transition away from the fee-for-service (FFS) model. A Brief History of Value-Based CareTo understand the evolution of value-based care, it makes sense to start with the Centers for Medicare and Medicaid Services (CMS). CMS provides a useful chart documenting the history. Notably, the move to value-based care didn’t begin with the Affordable Care Act (ACA) in 2010. If you need a starting point, it’s probably 2008, when CMS initiated the Medicare Improvements for Patients and Providers Act, better known as MIPPA. MIPPA instituted incentives for reporting quality data and e-prescribing. It set the stage for an array of other programs, all of which apply to physicians who accept Medicare, and the payments applied only to Medicare payments. In 2012:

In 2014:

And in 2015:

The ACA and ACOs The ACA accelerated value-based models; among its multitude of provisions was the Medicare Shared Savings Program, which created Accountable Care Organizations (ACOs). ACOs make participants — typically, clinicians, practices and hospitals — accountable for the health of their patients. Providers in ACOs receive financial incentives to coordinate care, reduce errors and avoid unnecessary tests and procedures. They also benefit from economies of scale. A successful ACO meets quality standards and yields savings, which are shared among payers and providers. In many models, an ACO shares risk, too: If it spends more than the targeted amount, it must repay some of the difference. Private insurers shortly followed suit, recognizing the benefits of value-based care in general and ACOs in particular. A Work in ProgressDespite all the progress with value-based care, FFS remains the dominant reimbursement model. It will likely remain so for several years, but value-based models continue to prove their value. FFS focuses on sick care — caring for patients after they become ill. The value-based care model focuses on health care and pays providers for the value of the care they provide, not the volume. And that’s the key point when considering value-based care vs. fee-for-service. Here are the main distinctions between the two models. 1. Volume vs. Value, Quantity vs. Quality Under FFS, clinicians, hospitals and medical practices are reimbursed based on the quantity of services delivered. More visits, tests and procedures mean more money. Spending more time with a patient or providing patient education hurts their income. Likewise, they aren’t paid to work with other providers to coordinate patient care. As a result, one provider doesn’t know what the other is doing, resulting in inefficient delivery and wasteful service duplication. With value-based care, payment is determined by the quality, not quantity, of services. Appropriateness of care, efficient use of resources and clinical outcomes dictate reimbursement, not how many patients can be seen in an eight-hour day. Practices focus more on advancing the Triple Aim — better care for individuals, improving population health management strategies and controlling health care costs. 2. Proactive vs. Reactive Value-based care supports proactive management of health: preventing illnesses and injuries or catching them at an earlier stage when they’re less expensive to treat. The point is to avert the use of services when possible. Providers are paid to keep patients out of the hospital and to ensure that each test is necessary. By contrast, FFS is reactive. Clinicians, practices and hospitals get paid more when patients use more services. The focus is on treating the sickness rather than keeping the person healthy. 3. Inside vs. Outside the Clinic Walls FFS focuses on what happens during the office visit or at the lab; it’s about the specific treatment or procedure. Value-based care takes a more holistic approach, looking at the patient and the patient population beyond the clinic walls. It’s proactive, focusing on prevention and even “nonvisit” care, such as providing health coaches. For diabetes, the patient might be connected with a nutritionist or set up with remote glucose monitoring. But, as the National Institute of Diabetes and Digestive and Kidney Diseases puts it rather bluntly, “Providing that care requires that a practice knows exactly who is receiving diabetes care.” That’s where data comes in. 4. Data-Driven Coordination vs. Working in the Dark In value-based care models, physicians have access not only to their own data, but also to patient data across the continuum of care (from labs to specialists, and so on). This gives them a better view of each patient and the patient population. With this data, they can identify all the patients who have a particular condition and those at risk for it. For example, that information can be used to determine which patients are at risk for diabetes. It can also be used to develop population-based interventions for every patient with diabetes. In contrast, FFS providers often lack the technology and the incentives to coordinate patient care across the continuum. Physicians are siloed, often lacking robust data on their own patient populations. And because they can’t see the tests run by other providers, they often duplicate procedures, like having a patient take a blood test for a second or third time. This coordinated vs. fragmented distinction may be the essence of value-based care vs. fee-for-service. It’s the efficient, data-supported, coordinated approach to care that delivers value by avoiding redundancy, leveraging economies of scale and working across the care continuum to keep your employees healthy. It’s health, not bean counting, that drives the savings. Visit with an online doctor from the comfort of your home and get expert advice, a treatment plan and a prescription if needed.  If you have kids, you probably know that child care tends to fall through at the most inconvenient moments.

This creates a stressful problem, and a costly one, too. According to the 2017 Child Care Aware of America Report, nearly half of working parents miss on average more than eight days of work a year because of breakdowns in child care. And for employers, that absenteeism gets expensive, to the tune of about $4.4 billion a year. Subsidizing Care: A Win-Win Investment That’s why supporting working parents isn’t just a generous thing to do for employee peace of mind — it’s a good investment in your workforce as a whole. And some businesses have caught on, offering employer-paid child care benefits that tackle four main areas: affordability, access, tax savings and workday flexibility. Starbucks is one company leading the charge. In October 2018, the company announced that it would subsidize 10 days of backup child care each year for all employees. The subsidy makes backup care much more affordable for in-home and in-center services at $1 and $5 per hour, respectively. Should you join them? The benefits of time and opportunity costs saved from missed work days make a compelling business case to do so, but according to a 2016 survey from the Society for Human Resource Management (SHRM), subsidized child care is still an underdog in the world of benefits. All told, just 2 percent of employers (big and small) reported offering the benefit, dwarfed even by the number of companies that offered day care at or near the work site (7 percent). Why the lack of participation? It’s simple: Many businesses, especially small ones, just can’t afford it — even though they’d like to, and even though they realize the impact those investments could have on their bottom line. If that sounds like you, don’t despair. The SHRM survey showed that there are other ways to go about supporting working parents. Other Solutions: Tax Savings and Care Finder Services Dependent Care Assistance Plans (DCAP), which allow employees to contribute pretax dollars for dependent care — much like health savings accounts do for health expenses — topped the list. About 56 percent of all employers in the SHRM survey reported that they offered DCAPs to employees, and 49 percent of small employers (50 to 99 employees) did so. Like health savings accounts, DCAPs offer a flexible option for employers. You can help contribute as much or as little as you want to employees’ accounts, and your workers reap the benefits in tax savings. With a 41 percent participation rate, child care location services (such as offering referral resources) were also popular, according to the SHRM survey. Other options trailing behind in the minority included summer child care, sick care and backup care. And Finally: Good Old-Fashioned Flexibility If none of these solutions piques your interest or meets your budget, simply building more flexibility into the workday can do a lot to help accommodate working parents. Consider flexible schedules that work around school pickup and drop-off times or work-from-home options for when child care falls through. Because inevitably, it will — and when it does, it’s best to have solutions in place for your employees that save their sanity and your bottom line. Explore small business health insurance plans and get the best plans for your business, if you want to know more details then please send your queries in the comment section.  Workplace wellness programs are a popular benefit, and for good reason — they’re an effective, engaging way to teach employees how to live healthier lives. But teaching employees how to improve their finances can be just as beneficial for their health, not to mention their pocketbooks. Here’s what your company has to gain from adding a financial education program to its offerings.

Financial Literacy and Health Financial literacy entails having the knowledge and confidence to handle money issues like managing debt, saving for retirement and setting a budget — things people need to deal with every day. Despite how important these topics are, according to Fortune, nearly two-thirds of Americans could not pass a quiz covering basic financial literacy concepts. Almost no one can say they’ve never worried about the bills, but serious financial stress can lead to health problems including depression, anxiety, trouble sleeping, high blood pressure and diabetes. Even worse, a low bank account balance might convince a sick employee that seeing their doctor or getting other important medical care isn’t worth the expense, even if they really need it. Financial stress also follows employees into work. When your employees are having trouble making ends meet, it’s nearly impossible for them to fully concentrate at work. The Society for Human Resource Management found that an employee’s personal financial issues can lead to an inability to focus at work and higher absenteeism. 4 Ways to Improve Employee Financial Knowledge If you’re interested in improving your employees’ financial skills, here are a few tried-and-true strategies to have in your back pocket.

Maximizing Health Insurance Benefits Covering your health insurance plan as part of your financial literacy training will help employees get the most out of one of the key benefits included in their package. At a minimum, you should remind everyone about how they can reduce their health care costs by looking for in-network providers, following up with preventive treatment and using generic prescriptions when possible. As you discuss budgeting, show examples of how much different trips to the doctor or hospital could cost employees under your plan’s current structure for deductibles and copays. Then, discuss strategies for how employees can save part of their income to prepare for these costs. If your health offerings include extra features like a flexible spending account (FSA) or health savings account (HSA), your financial literacy program might benefit from a workshop or seminar explaining how these more complicated programs work. For example, make sure employees know that the money in an FSA follows a “use it or lose it” policy and might be lost at the end of the year. Promoting financial wellness is a small investment on your end, but it can greatly improve the finances, health and productivity of your employees, so don’t overlook this workplace benefit in your office. When your employees are financially well, they’ll pour less of their energy into stressing over bills and more of it into making your business successful. Explore health insurance plans harrisburg and get the best plans for your family, if you want to know more details then please send your queries in the comment section.  When one of your employees gets a new diagnosis, especially an unexpected one, their worrying doesn’t stop as they leave the hospital. They’ll carry that stress with them at home, as they run errands and, of course, at work.

As an employer, it can be tough to know how to help someone coping with a diagnosis — whether it’s their own or a family member’s — but as difficult as it may be, letting your workforce know you’re there to be a supportive presence could have a big impact on their mental state and their productivity and they navigate treatment and recovery. Try out the following seven tips to ensure you’re prepared to begin supporting employees through a tough time, whatever their situation is. 1. Respect Their Privacy Legally, an employee doesn’t have to tell you that they or a family member received a new diagnosis. Let them come to you in their own time to share the details, and ask how or if they want the news to be shared with colleagues. Once they’ve answered, respect their decision. 2. Direct Them to the Right Benefits Make sure the employee has someone to talk to who can thoroughly explain all of the benefits available to them, including health insurance, short-term disability, the Family and Medical Leave Act, counseling services, an employee assistance program and any other benefits you may have in place. 3. Be Flexible With Scheduling Some diagnoses might not change an employee’s schedule much, but others can require time-consuming treatments and appointments. As much as possible, discuss ways you can adjust their schedule to accommodate treatment and recovery. Can some client meetings be conducted through a video conference rather than in person? Can the employee work from home during specific treatments or during their overall recovery period? Can their core hours be shifted to accommodate appointments? 4. Create a Plan for Work A newly diagnosed employee might worry about not getting all their work done, but that kind of added stress will only slow down their recovery. Take the lead in developing a schedule to determine what tasks need prioritizing, what can be delayed and what should be delegated to someone else. 5. Give Them Space Answering calls from a doctor about test results or other confidential medical information can be awkward in an open office environment, especially if an employee is keeping their condition private. Offer up your office or another quiet, separate area as a space to take phone calls. Small gestures like this can do a lot to maintain morale and make your entire staff feel supported. 6. Guide Co-Workers in How to Help If the employee chooses to share their diagnosis with others, they may find themselves overwhelmed as everyone jumps in to help. While your employees’ thoughtfulness is obviously a positive thing, try to direct their energy in a more useful way. Ask what would be most beneficial to the employee with the health concern, and tell your staff how and when they can assist. For instance, you might send around a sign-up sheet with different opportunities to help, such as bringing in a meal, doing chores, donating vacation hours or raising money to cover medical costs. That way, their efforts will all go toward the right things. 7. Check In With Encouragement Calls, texts or cards just checking in and hoping for a quick recovery let the employee know you care. Just make sure not to mention work — there’s a better time and place for those conversations (namely, at work). Work is a source of stress for many Americans — but when an employee is facing a new diagnosis, you can flip the script and turn the workplace into somewhere they feel supported. This can improve morale, giving the struggling employee an emotional boost that can aid their recovery. As an employer, you have an opportunity every day to decide what kind of business you want to run and how it treats the people who work to keep the company successful. It just makes sense to make coping with a diagnosis as easy for them as possible. Explore business health insurance plans and get the best plans for your company, if you want to know more details then please send your queries in the comment section. |