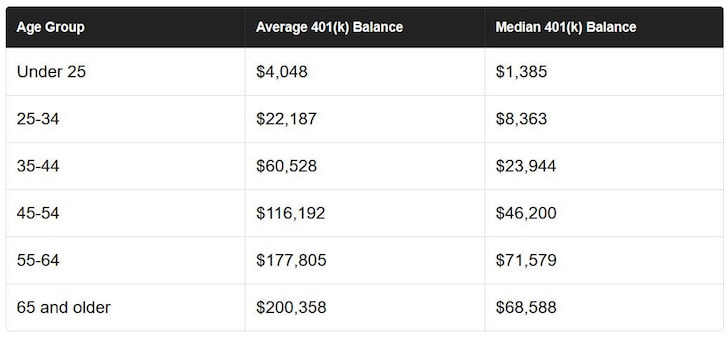

You likely won’t be able to live off your 401(k) alone in retirement, but you should be able to combine your 401(k) with alternative savings, other passive investments, and Social Security to live a financially free life when the time comes to withdraw at the age of 59.5. Most Americans don’t have pensions. The reality is that the median account balance in the U.S. is only around $72,000 for 55-64 year olds in 2019 according to Vanguard, one of the largest 401k managers. The average 401k balance for 55-64 year olds is roughly $178,000. But the average is screwed up to due the super wealthy. Even with $178,000 in your 401k at retirement age, you aren’t going to be living it up for the next 20 – 30 years without alternative sources of income.  According to data from Fidelity, here’s the average 401k breakdown by age in 2018:

Ages 20 – 29: $9,900 Ages 30 – 39: $38,400 Ages 40 – 49: $91,000 Ages 50 – 59: $152,700 Ages 60 – 69: $167,700 Ages 70 – 79: $160,200 Given the median age of Americans is 35.3 according to the US Census Bureau, the median 401(k) balance per person should be closer to $150,000 – $500,000 according to my 401(k) retirement savings guide instead of these pitifully low levels. In this article, I’d like to share some stories on what happened to all the missing savings because we all know we should be maxing out our 401k every year for as long as we work. Financial Samurai 401k Savings GuidelineThe below chart shows what a typical 22 year old college graduate should have accumulated in their 401(k) if they followed my advice and started maxing out their 401(k) after two years of working. The maximum pre-tax contribution amount is $19,000 in 2019 and will likely increase by $500 a year every couple of years to keep up with inflation. I’ve divided the chart into three columns to account for older savers, middle age savers, and younger saves due to the different maximum contribution limits. I’ve also accounted for different return and company matching metrics. The bottom line: everybody who consistently contributes to their 401k over a 38 year career will likely have at least $1,000,000 in their account. The 401k savings targets by age can also act as a total savings guideline as well if you wish. 401k By Age Discrepancies Explained I’ve been consulting with more clients about their personal finances and what I’ve discovered is that something always seems to come up and knock someone off their retirement savings path. It’s all fine and dandy to assume everyone should logically max out their 401(k) or at least save 20% of their after tax income until retirement, but this is seldom the case. With consent from my clients, let me share several case studies to illustrate some points. I’ll also highlight one reader’s e-mail feedback about the topic as well as my own example. Names are changed for privacy reasons. Case Study One – Family To Support Joe is 42 years old and makes $120,000 a year as an engineer. He’s been working for 19 years and has $80,000 in his 401(k) (vs $300,000+ recommended). When I asked him to share his 401(k) situation he shrugged. He never considered maxing out his 401(k) because he always thought he wouldn’t have enough money left to take care for his wife and son. His wife worked for the first eight years and decided to stay at home after giving birth. Going from a two income family to a one income family is difficult if you’re not use to saving half. Joe has about $12,000 in after-tax savings which will cover about four months of living expenses just in case something bad happens. Given the thin buffer, we talked about the importance of getting long term disability. When I dug deeper, I realized Joe has a penchant for fixing up old cars. All told, he’s spent over $60,000 after taxes to beautify his two 1965 Mustangs. Case Study Two – Expensive Living Sally is 32 years old, and makes $75,000 + bonus as a medical equipment sales rep. Sally got her Master’s degree in healthcare, and graduated with $27,000 in debt at the age of 24. She pays about $500 a month in student loans which she plans to pay off in 10 years tops. After seven and a half years of working at a reputable firm, Sally has $70,000 in her 401(k) compared to a recommended $127,000 after eight years of work experience according to my guide. Sally only contributed 10% of her annual gross salary into her 401(k) because of her school debt, car payments, credit card payments, and $2,600 a month rent here in San Francisco. Sally’s case shows that education is expensive and good paying jobs come with higher cost of living. Sally has about $5,000 in savings in the bank. Case Study Three – High Income Burnout Susie is 34 years old, single and makes $150,000 + bonus as a VP at an investment bank based in San Francisco. She’s been working for 12 consecutive years out of college. In between years 10 and 12, Susie took a 1.5 year hiatus to become a baker during the financial crisis. She was burned out and wanted to try something new. But, after spending $25,000 for tuition, missing out on 1.5 years worth of income, and getting screamed at while making only $10 an hour, she realized being a baker at a restaurant was not for her. “If I’m going to get yelled at making $10 an hour, I might as well make a lot of money!” Susie joked. Susie has about $150,000 in her 401(k), 50% higher than the current median according to Transamerica. However, given she didn’t earn any money for 1.5 years and payed a lot for tuition, Susie is also about $50,000 light based on my guide. Susie was only contributing about 10% of her pre-tax income to her 401(k) for her entire career because she didn’t want to tie her money up beyond the company match. Case Study Four – Highly Educated Couple An e-mail from a reader responding to the Average Net Worth For The Above Average Person article: “I noticed that most of your posts are geared towards people who start working at age 22 with minimal debt – as just one example, your “above average” people projections. But many “above average” people do not start working at age 22 and incur substantial debt before they start working. For example, I am a lawyer that obtained a master’s degree and then a law degree before starting my career at age 28. My wife is a doctor, who completed her residency and started practicing at age 28 as well. Both of us started our careers with substantial student loan burdens – over $325,000 between the both of us. Our late start means we lose a lot of the magic of compounding interest. And our debt burden takes a big chunk of our monthly income. These are significant challenges.” Case Study Five – Early Retiree My 401(k) was about $400,000 when I left work at age 34 in 2012. It has grown to about $550,000 in 2019. What I miss about work was my $20,000 – $25,000 a year in profit sharing. That addition was a huge boost to my annual 401(k) that cannot be underestimated. It was only until 2014 when I realized I could open up a Solo 401(k) with the freelance income I was generating. My Solo 401(k) now has about $200,000. Case Study Six – A Nasty Divorce! A reader shares his story, What is misleading as to why many 401k’s are half or less what they should be is one word…DIVORCE. I am currently 44 yrs old. 7 years ago at age 37 I had $125,000 in my 401k and then….BOOM! Stock market crashed and my 401k was worth $80,000. Yeah not fun. 7 years later it has now recovered but that’s lost years and now my 401k is worth $130,000 and I’m getting divorced and half goes to my wife. Now I’m back to $65,000. Ridiculous. Over 50% of married couples get divorced and many men are paying Child Support and Alimony and aside from losing half our retirement we now have nothing for years to invest…but I digress.” Case Study Seven – Medical Debt Medical debt is one of the leading causes of bankruptcy in America. Deena, 51, explains, “I have a rare disease and nearly died (which means time in the ICU, operations, and 1 – 6 month recovery where I work part time or not at all) in 1995, 97, 99, 02, 03, 05, 06, and 07. Then I met the love of my life, who had ovarian cancer and passed away after 4 painful years. Because she was the wrong gender, we could not legally get married, so her insurance and medical costs were in the hundred of thousands of dollars. Medical debt on top of not being able to work is a huge factor that needs to be considered. After 10 years, I have just finished paying off both of our medical debt.” Technical Reasons Why 401(k) Balances Are So LowNow that we’ve heard from seven different case studies why their 401(k) balances are so low, let’s look into some technical reasons as well. Four aspects of the U.S. retirement system could explain the discrepancy between potential and actual accumulations at age 60. • First, the immaturity of the 401(k) system means that many 60-year-olds did not have access to a 401(k) plan early on in their careers, so they would have accumulated less than workers covered throughout their work lives. • Second, the lack of universal coverage means that workers are not always in jobs that offer retirement plans and, therefore, are not always able to contribute. • Third, participants’ ability to tap their account before retirement means that accumulations leak out. • Fourth, fees can significantly erode net returns on investments. Life Happens To Us AllWe all know we should be maxing out your 401(k)s but don’t because something always seems to get in the way. Life gets in the way of our retirement savings plans all the time. We have tuition to pay, expensive cars to fix, vacations to take, concerts to attend, shoes to buy, Range Rover Superchargers to drive, alimony to pay, sickness to deal with and economic dislocations to experience. Here’s another chart comparing the median and average 401(k) balance by age and my 401(k) guidance if we continuously max out your 401(k) each year. Some of us just like to honestly blow lots of money and not give a damn! There’s always an excuse for not saving. However, if you don’t want to become one of those tragedy stories or a burden to your fellow citizens, then I suggest increasing your 401(k) contributions and after tax savings percentages. If the amount you are savings doesn’t hurt, then you are not saving enough. At the end of our careers, we only have ourselves to blame if we come up short. Unless you have developed alternative income streams, paid off your house, and have other after tax savings, living off $350,000-$500,000 for the next 20-30 years is just $12,000 – $25,000 a year. Pay yourself first before anything else and max out your 401K. After you’ve maxed out your 401(k), figure out where you can save some more in your after-tax investment accounts to generate passive income. You can no longer count on a pension or Social Security to support you in retirement. The only thing you can count on for living a comfortable retirement is you! Recommendation To Grow Your Net Worth Manage Your Finances In One Place: The best way to build wealth is to get a handle on your finances by signing up with Personal Capital. They are a free online platform which aggregates all your financial accounts on their Dashboard so you can see where you can optimize. Before Personal Capital, I had to log into eight different systems to track 28 different accounts (brokerage, multiple banks, 401K, etc) to track my finances. Now, I can just log into Personal Capital to see how my stock accounts are doing, how my net worth is progressing, and where my spending is going. One of their best tools is the 401K/Portfolio Fee Analyzer which has helped me save over $1,700 in annual portfolio fees I had no idea I was paying. You just click on the Investment Tab and run your portfolio through their fee analyzer with one click of the button. Another awesome feature is their Retirement Planning Calculator which uses your real inputs to run a Monte Carlo simulation to best estimate your retirement financials. Definitely see how you stand! Author Bio: Sam started Financial Samurai in 2009 to help people achieve financial freedom sooner, rather than later. He spent 13 years working in investment banking, earned his MBA from UC Berkeley, and retired at age 34 in San Francisco in 2012. To stay on top of your wealth, Sam recommends signing up with Personal Capital’s free financial tools. With Personal Capital, you can track your cash flow, x-ray your investments for excessive fees, and make sure your retirement plans are on track. For 2019 and beyond, Sam is most interested in investing in the heartland of America where real estate valuations are much lower and net rental yields are much higher. Interest rates have plummeted to 2-year lows and demand for real estate remains strong. Fundrise is his favorite real estate crowdfunding platform. It’s free to sign up and explore. Explore best health insurance harrisburg and get the best plans for your family, if you want to know more details then please send your queries in the comment section.

1 Comment

14/10/2019 11:44:13 pm

Medical debt is one of the leading causes of bankruptcy in America. Leave a Reply. |